Convert Tax Liability into Energy Investments

The Final Turn AFE Acquisition Fund provides accredited investors access to non-operated working interests designed to deliver substantial first-year tax deductions and long term cash flow potential.

Why Investors Should Consider Final Turn

Tax Efficiency

Targeting 60-80% of invested capital qualifying for ordinary income offsets in the first year.

Cash Flow

Quarterly distributions expected to begin in year 2 as wells start to produce.

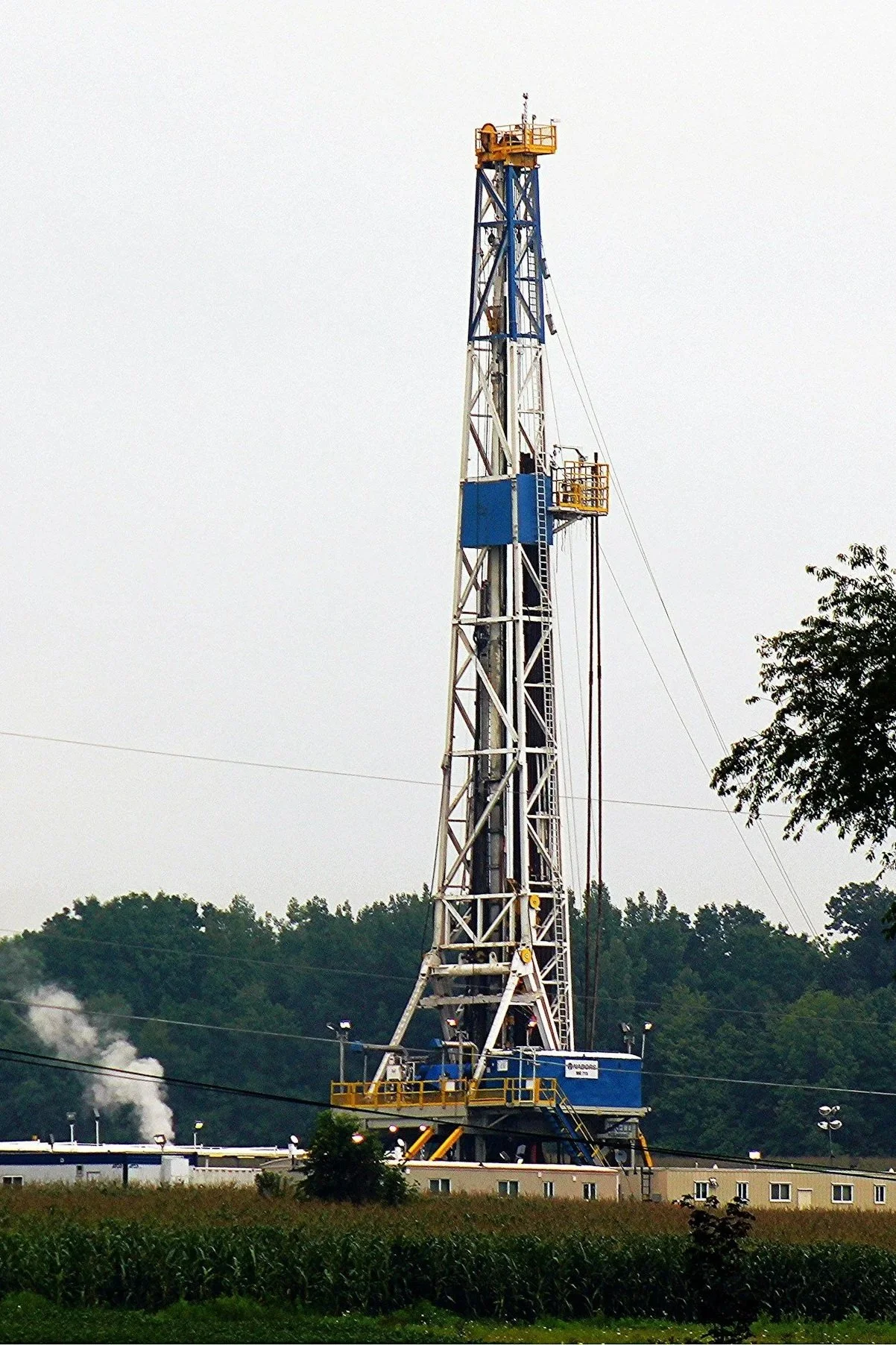

Direct Asset Ownership

Fractional ownership interest in the drilling, completion, and production of oil & gas wells.

Hands-Off Ownership

Participate directly in oil & gas drilling projects without having to manage day-to-day operations.

How It Works

Capital is committed to Final Turn.

Step 1

Final Turn acquires minority working interests in drilling opportunities.

Step 2

Investors receive their proportionate share of year 1 tax benefits associated with the drilling and completion activities.

Step 3

Wells begin to produce hydrocarbons and Final Turn receives its proportionate share of cashflow from each well.

Step 4

Step 5

Cash distributions are made to investors.

Key Tax Benefits Explained

-

IRC 469(c)(3) is the foundational provision that allows non-operated working interest to offset ordinary income (W2, 1099, bonuses, etc).

States that a working interest in an oil or gas property is treated as a non-passive activity but applies only when the interest is held directly or through a general partner structure.

-

IRC 263(c) allows taxpayers with a working interest to elect to expense 100% of the intangible drilling costs in the year incurred.

Intangible costs generally make up ~80% of the development cost and applies to items with no salvage value (labor, services, fuel, etc.)

-

Tangible well equipment (pipe, pumps, facilities, etc.) can be capitalized and depreciated under MACRS.

Passing of the Big Beautiful Bill in 2025 re-instated tangible costs for oil & gas wells as qualifying property, therefore making the costs eligible for year 1 bonus depreciation.

IRC 167 - Depreciation / IRC 168 - MACRS / IRC 168(k) - Bonus Depreciation

-

IRC 613 allows for 15% of properties gross income each year to be sheltered from income tax (subject to certain limits).

Total depletion allowed over time can exceed the investor’s original capital investment and continues after capital costs have been recovered.

Disclaimer: This website is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering will be made solely through the fund's governing and offering documents, which will control in all cases. Tax benefits and investment outcomes are not guaranteed and will vary based on individual circumstances. Prospective investors should consult their own tax advisor, attorney, and financial professional before making any investment decision.